Every Function Delivered. Enterprise Value Didn’t.

Why operating decisions destroy economic profit when no single unit prices the trade-offs.

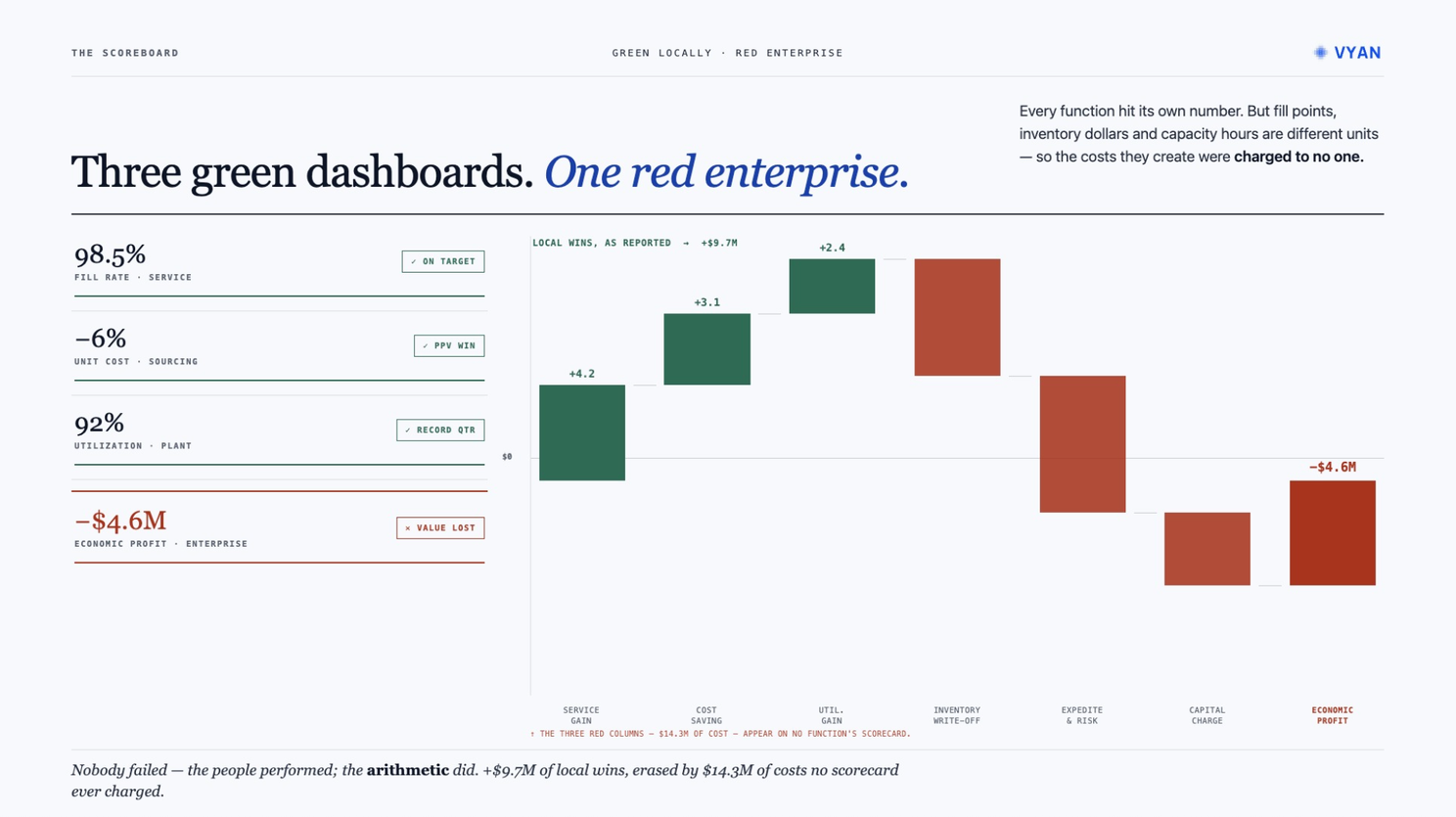

Here is a quarter most leaders will recognize. Service hit 98.5% fill — on target. Sourcing delivered a 6% unit-cost reduction — a purchasing win. The plant ran at 92% utilization — a record. Three dashboards, all green, all defensible, every function a hero.

And the enterprise lost money. Negative economic profit for the quarter.

Nobody failed. The people performed; the arithmetic did. Fill points, inventory dollars, and capacity hours are different units — so when service holds a buffer, when sourcing buys ahead to land the discount, when the plant runs hot to post its number, the costs they create get charged to no one. The local wins were real — about +$9.7M of them. The costs no scorecard ever showed were larger — roughly $14.3M in write-offs, expedites, disruption exposure, and the capital charge on all of it.

Three green dashboards summing to one red enterprise is not a measurement glitch. It is what happens when an organization optimizes the parts it can score and never prices the whole.

So the real question is not how to measure each function better. It is what it would take to price the whole — in one currency, at the moment you decide.

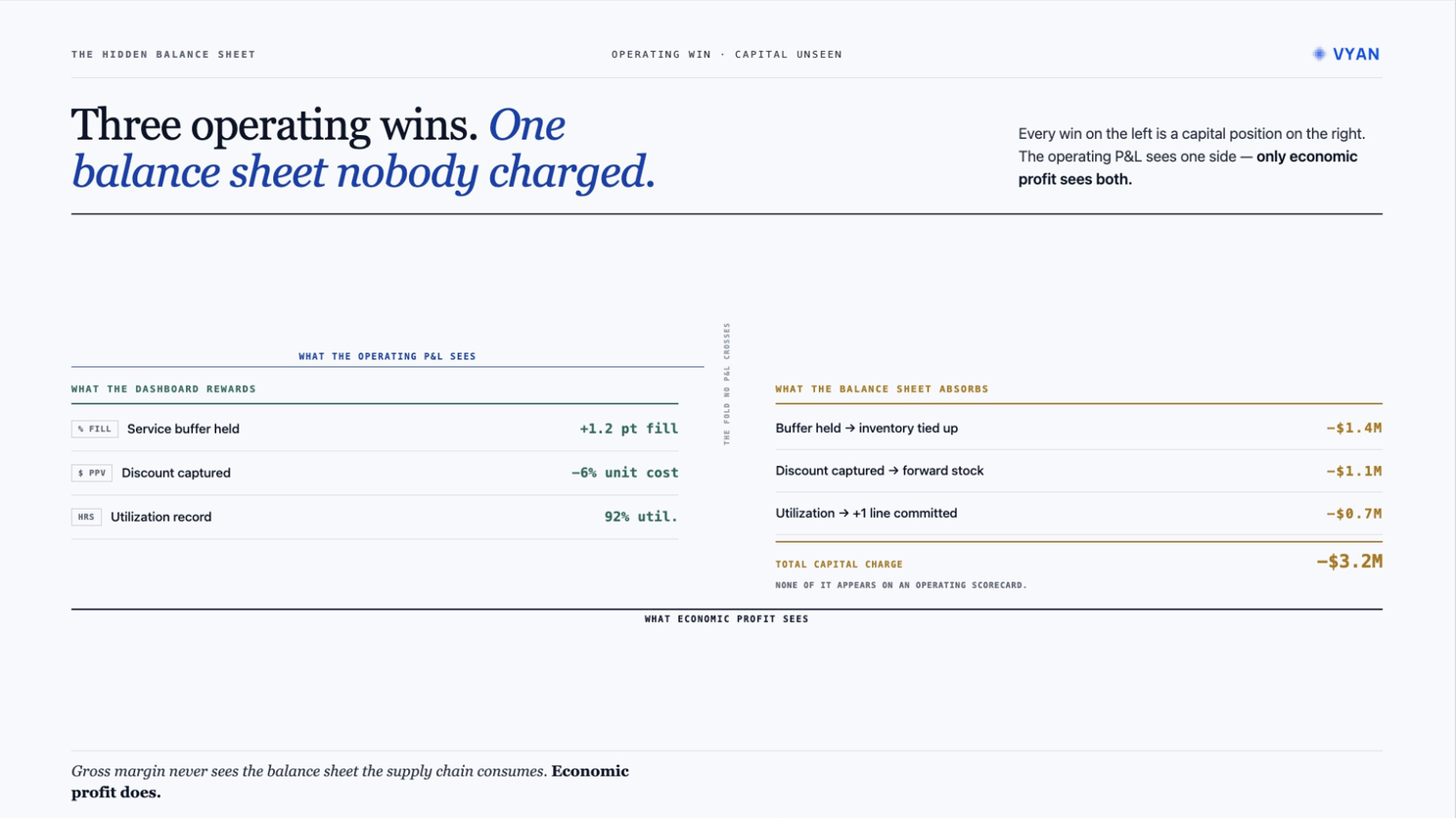

And the reason the whole goes unpriced is structural. The supply chain's biggest levers — inventory, capacity, footprint — are capital bets dressed as operating choices. A service buffer held, a discount captured by buying ahead, a utilization record posted by running the plant hot: each lands on an operating dashboard as a win, and each quietly ties up capital on a balance sheet no operating scorecard ever reads. Gross margin never sees it. The capital charge is real, it is large, and it is invisible to every metric the operating floor actually manages to.

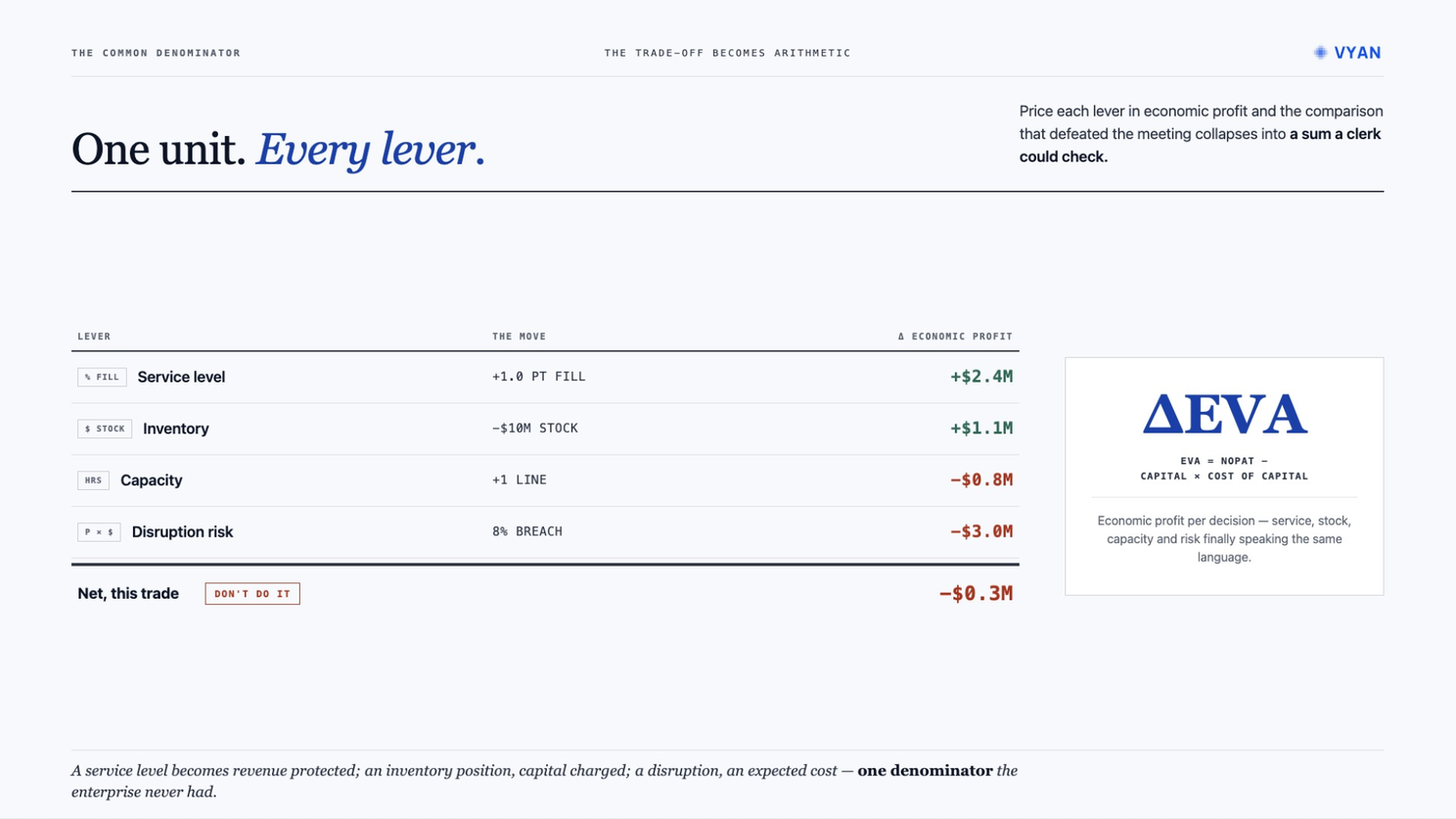

There is a number that does this, and its distinguishing feature is the one most operating metrics ignore: it charges for capital. Economic Value Added — economic profit after the cost of the capital employed — converts every lever into the same currency. A service level stops being a percentage and becomes revenue protected. An inventory position stops being a stock figure and becomes capital charged. A disruption stops being a risk-register entry and becomes an expected cost.

This is why EVA, and not gross margin or contribution or fill rate, is the right common denominator for operating decisions. The supply chain's biggest levers — inventory, capacity, footprint — are capital bets dressed as operating choices. Gross margin never sees the balance sheet they consume. EVA does. It is the only unit in which a buffer, a discount, and a utilization record can be added up and compared.

Once every lever speaks in that unit, the trade-off that defeated the meeting collapses into a sum: this move adds $2.4M, that one frees $1.1M, this one costs $0.8M, that exposure runs $3.0M — net, don't do it. The comparison that used to require the loudest voice in the room now requires arithmetic.

If this sounds familiar, it should. EVA is not new. A generation of companies adopted it and most quietly let it fade — and that history points straight at why it can work now when it didn't then. EVA struggled as a periodic scorecard: computed by hand, long after the decisions it was meant to govern, reported to finance and filed. It was the right unit, arriving too late to change anything.

What is new is not the metric. It is the ability to compute it across every lever, fast enough to decide with — before the buffer is held, before the discount is taken, before the plant is told to run hot. EVA stops being a reporting metric you review after the quarter closes and becomes a decision metric you compute before you commit. That shift — from after to before — is the entire move.

A fair objection follows: run a company on one number and you will game it — defer the capex, starve the brand, run the assets hot to dodge the capital charge. The risk is real, and it is exactly why EVA is the objective, not the whole policy. The floors a business must hold — service, margin, cash, the strategic bets leadership makes deliberately — are constraints the decision is required to respect, not variables it is free to trade away. EVA chooses among the options that already clear the floors. Where to set those floors stays with the executives it belongs to. What leaves the room is the arithmetic, which never belonged there.

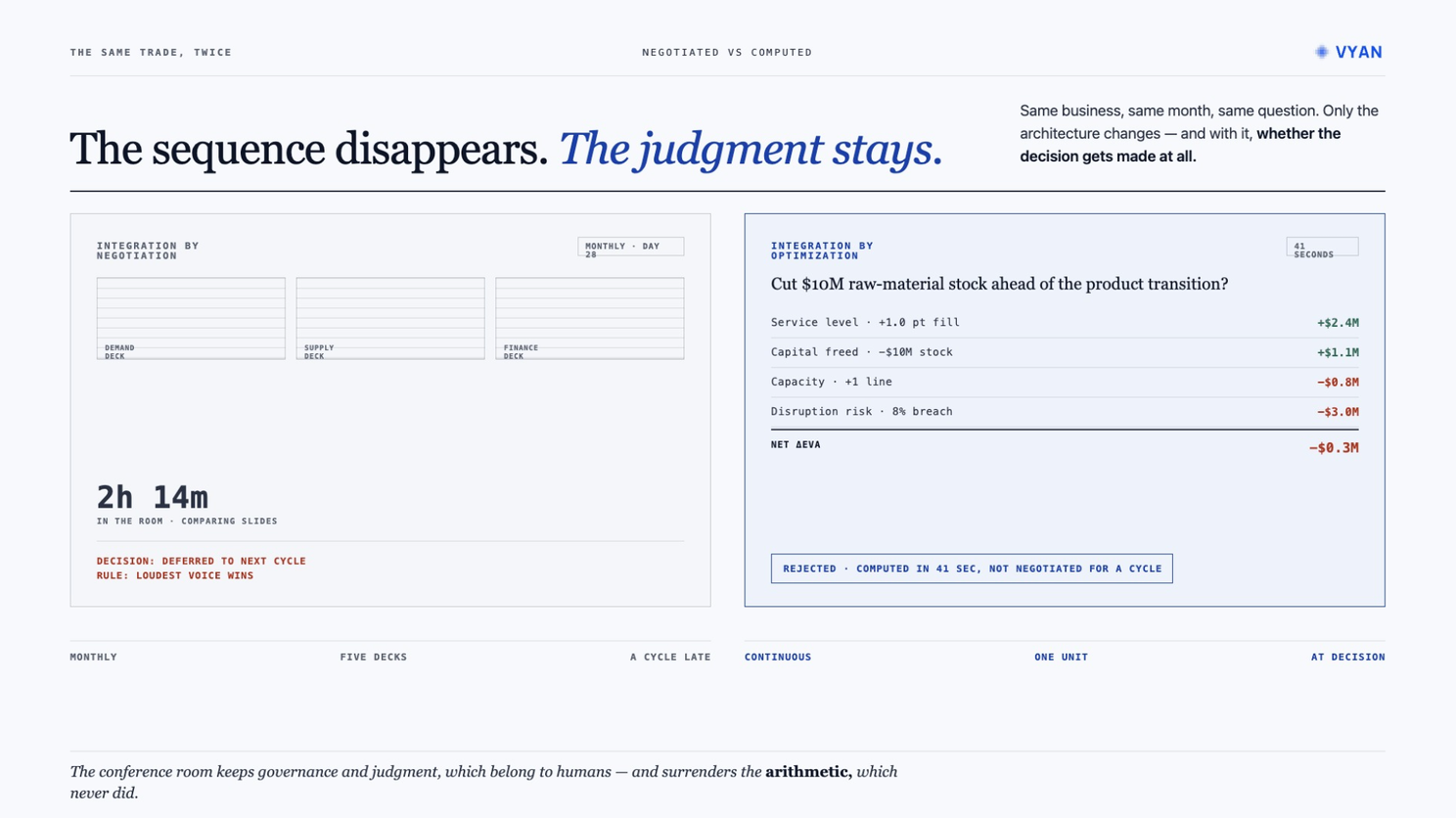

Put the two architectures on the same decision: cut $10M of raw-material stock ahead of a product transition? In the meeting, that question costs two hours of comparing slides across demand, supply, and finance, then defers to next cycle, decided by whoever pushed hardest. Priced in one unit across service, capital, capacity, and risk, the same question is netted and answered — rejected — in under a minute. The sequence disappears. The judgment stays.

The fix is not a better forecast or another dashboard. It is a change of architecture: stop reconciling five local optima in a room once a month, and start solving one problem in one unit, continuously — the executive setting the floors, the system pricing every trade-off at the moment of decision. Plans break because they optimize one function's number in one function's unit. A policy holds because it prices the whole, in the one currency that counts the capital.

None of this is theory. One company — a conglomerate founded in 1897, whose products reach over a billion people — put EVA in front of its operating people and ran on it for the better part of two decades. Not as a finance-department scorecard, but as the number behind promotions, capacity, overtime, outsourcing, and capital requests, in the hands of people who never opened a finance textbook. Sustaining that is far rarer than adopting it. What it took to hold — the incentives, the discipline, and the turn the story takes in its second decade — is the most honest account you will hear of running a company on economic profit.

On July 14, I am hosting a fireside with Dr. Rakesh Sinha, who spent 39 years at Godrej and ran operating decisions on EVA from the operating seat. If the quarter above looked familiar, it is worth an hour.

July 14 — reserve a seat: https://vyan.ai/webinars/eva-fireside-rakesh-sinha